Everyone has been talking about mortgage rates over the past year.

Month after month, they continued to hit new historic lows in 2020.

While mortgage rates remain low, they are beginning to fluctuate. Mark Fleming, Chief Economist at First American, said,

“Although they remain low, mortgage rates have begun to increase and are expected to rise further later in the year, thus affordability will test buyer demand in the months ahead and likely help slow the pace of price growth.”

If you are wondering exactly how much interest rates affect your monthly payment - keep reading to find out!

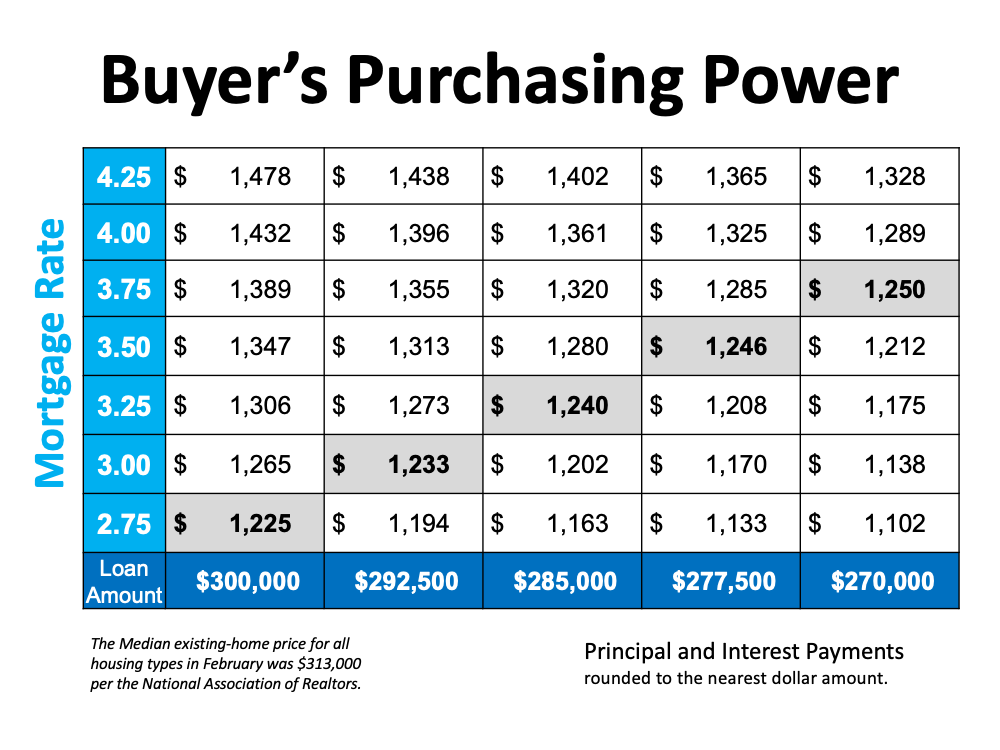

The truth is, even slight changes in mortgage rates make a difference in your monthly payment.

In the example above, you can see how an increase of 1% in interest rates changes your payments. If you want to keep you monthly payment for principal and interest between $1,200 and $1,250, you can afford a loan amount of $300,000 with a 2.75% interest rate. If that interest rate increases to 3.75%, the loan amount decreases to $270,000 in order to stay within your desired monthly payment.

This means that every time the mortgage rate increases, you need to look at lower-priced homes to stay within your desired budget.

Experts predict that rates will continue to rise modestly throughout 2021. Of course, just because mortgage rates are low, doesn’t mean you should overpay for a home. If you are planning on buying, make sure you work with a real estate agent who can help you set realistic expectations while finding a home that meets your needs.